An Easy to Catch (And Devastating) Research Hit

Some op research nuggets uniquely combine ease of discovery and powerful effectiveness when heard by voters.

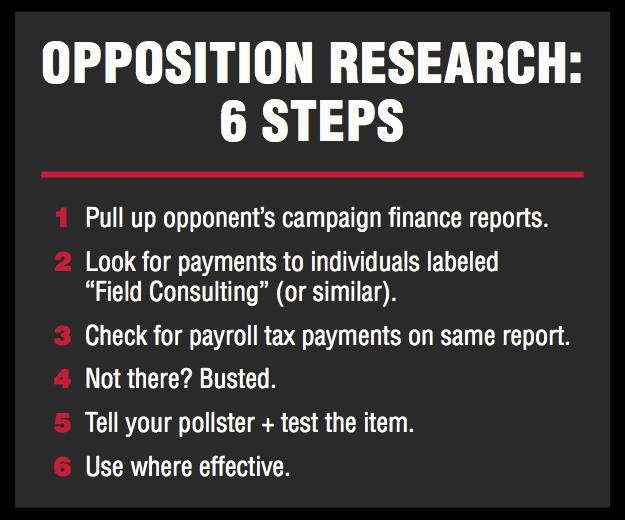

In the world of professional door-to-door field operations, from time to time, we see campaigns using 1099, or “contract labor,” to run their grassroots efforts.

These campaigns have a certain look and feel to us and when we check their campaign finance reports, we inevitably see “Field Consulting” or something of the sort next to out-payments to individual campaign workers, who are doing the actual door-to-door canvassing work.

Use of “contract labor” for this type of work is considered payroll tax fraud by the IRS and there are no exceptions or loopholes on this one: no matter how clever people think they are. It’s tax fraud pure and simple.

“An individual is an independent contractor if the payer has the right to control or direct only the result of the work and not what will be done and how it will be done.” That’s direct from the IRS.

It means that you can hire someone and not pay payroll taxes for them if and only if you never tell them how to do their job, where to go, what literature to pass out, what to say to voters, etc. They have to be the true expert in the equation in order to qualify as a 1099.

You know any canvassers like that? People you hire to canvass, but to whom you give zero direction? No? We don’t either. Which makes canvassing and most campaign staff roles, in fact, employee roles (W2s) and not eligible for 1099 treatment.

Additionally, if the payer has any control over how the worker is paid (what terms), whether they get reimbursed for expenses, who’s providing tools and supplies. If the answer to any of these is, “the campaign is dictating terms for these things,” then cha ching, that’s an employee, not a contractor, and the IRS will chase you down for payroll taxes owed, and in some cases assign penalties or jail time.

At a recent conclave of the Republican Lawyers Association in Denver, the topic of “contract labor” and its use was discussed at length and the attorneys were adamant that this is clear cut.

Generally speaking, voters don’t react well to the candidates running for office who side-step their responsibilities vis-a-vis paying their taxes.

Republican and Democratic voters alike believe that they themselves are struggling to pay what’s asked and they don’t care for politicians who don’t.

One pollster I asked commented that this hit is particularly effective with GOP leaners and Independent voters, who according to him, “see the issue as something a typical politician would do, force everyone else to pay, but don’t do it themselves. It manifests the whole ‘the system is broken’ narrative.”

At our firm, we tend to believe that campaigns or vendor firms transgress less because they are hoping to avoid the expense of payroll taxes and more because they don’t want to or just don’t have the ability to deal with the difficulties of actually managing payroll for all these canvassers or having to address issues of insurance and legal liability.

Basically, campaigns or field operations vendors that push the use of 1099 contractors just can’t effectively do what it takes to perform the functions of cutting checks to staff, calculating federal, state, and sometimes local taxes, worker’s comp coverage, and liability coverage.

In some cases, we can imagine that tax avoidance could have come into play as a result of a competitive bid process for a particular contract — as a means for a vendor to low ball on price.

Regardless of the motivation, the hit is easy to see, it’s super clear cut, and can be very effective. Highlighting it will at the very least cause chaos within the internal operations of your opponent’s campaign for a few days. Could generate some embarrassing press coverage, too. And that’s never a bad thing so long as you’re the one on the right side of the story.